The Pivotal Role of the Bank of Canada

At the core of the Canadian mortgage lending environment is the Bank of Canada (BoC) overnight mortgage loan. It serves as a benchmark for a range of lending rates across the country, including mortgages (Source 1). BoC’s primary objective is continuity has maintained stable prices, targeting inflation at around 2% per annum (Source 2). By adjusting the overnight rate, the central bank influences borrowing costs and ultimately consumer spending, to meet its growth target and drive employment surface (source 2).

Mortgage Rate Determinants

Many factors determine the cost of rent in Canada. First, the overnight pricing of the BoC directly affects the prime rate charged by commercial banks, which affects the variable cost of adjustable mortgages (Source 1, Source 2). Second, government bond yields are a measure of mortgage rates, with bond yields generally rising Generates Mortgage Prices (Source 1). Additionally, lenders consider factors such as the type of mortgage (purchase, refinance, or renewal), the borrower’s down payment, credit score, debt and income, and asset characteristics when determining interest rates (Source 1).

Mortgage Types and Rates

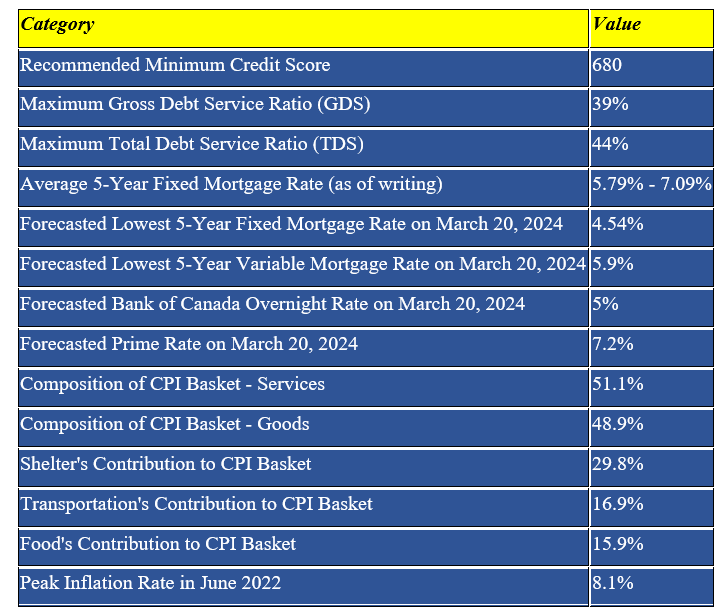

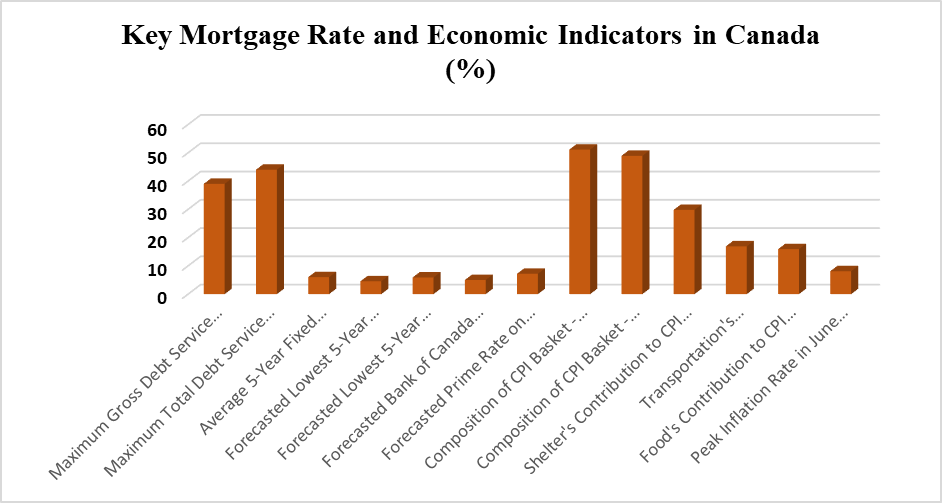

Canadian borrowers have a choice between fixed and variable loans. Fixed-rate mortgages provide predictability, where interest rates remain constant throughout, regardless of market fluctuations (Source 1). According to recent data, 5-year fixed mortgage rates offered by selected lenders range from 5.79% to 7.09% (Source 1). In other words, changes in the prime rate have a direct effect on the variable rent, and the interest rate is adjusted accordingly (Source 1).

Forecasting Mortgage Rates in 2024

Forward short-term borrowing rates through March 15, 2024, indicate the possibility of a decline in mortgage rates by the end of the year (source 2). Forecasts show that the minimum 5-year fixed mortgage rate could fall to 4.31% by 31 December 2024. While the 5-year variable rate could reach 5.2% (source 2). But this forecast could change depending on the market conditions and BoC’s on monetary policy decisions.

The Impact of Inflation and Economic Conditions

Inflation plays an important role in setting rent prices, while the BoC adjusts its overnight rates to maintain price stability (source 2). During periods of inflation, the central bank typically raises interest rates to control consumer spending and reduce demand, ultimately reducing prices (source 2). Conversely, if inflation exceeds the target, it may lower the BOC level to encourage economic activity and increase employment (source 2). The composition of the Consumer Price Index (CPI) basket, which includes goods and services such as accommodation (29.8%), transport (16.9%) and food (15.9%), also influences the BoC’s policy decisions (source 2).

Strategies for Finding the Right Mortgage Rate

To get a better mortgage in Canada, borrowers need to consider different options. These include improving their credit scores and costs and income (source 1). It saves money for larger down payments (source 1, source 3). It can also seek out government-backed programs that FHA and VA loans (source 3). Additionally, manipulation of the market by buying during periods of low interest rates can lead to significant savings over the life of the mortgage (Source 1, Source 3).

By understanding the dynamics of the Canadian mortgage landscape, including the role of the BoC, financial products and available mortgage options, borrowers can make informed decisions and thousands of dollars can be saved in interest costs.

Sources

https://www.forbes.com/advisor/ca/mortgages/best-mortgage-rates-in-canada/

https://wowa.ca/mortgage-interest-rates-forecast-2024

https://www.nesto.ca/mortgage-basics/mortgage-rates-forecast-canada/