As the Canadian economy navigates the uncharted waters of a post-pandemic recovery, variable lending and lending models – have emerged as a key factor shaping investment decisions for homeowners. The prime rate landscape is poised for dramatic change by 2024 and understanding the implications of these changes is critical to making informed choices.

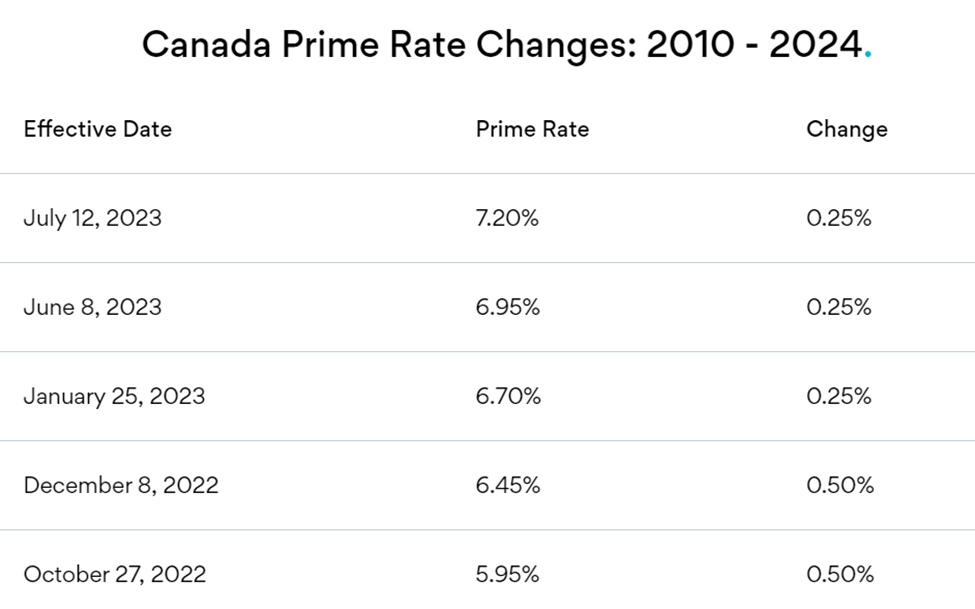

After a severe period when the Bank of Canada (BoC) imposed sharply higher interest rates to deal with inflation, the current record rate is 7.2% (2). But when inflation is showing signs of weakening, market experts predict that the BoC will initiate a series of rate cuts, potentially Starting as early as mid-2024 (1). This change in monetary policy is expected to have an impact covering a wide range of sectors, particularly housing markets and economic conditions.

For homeowners struggling with mortgage modifications, the anticipated discount could bring much-needed relief. As prime rates decline, their mortgage payments will follow, easing much of the fiscal pressure created by the sharp rate increases of the past two years (2). But it is important to note that not all variable-rate mortgages are created equal. Those who are able to adjust their payments are already feeling the impact of rising rates, while fixed payers could face a more costly renewal transition if they have defaulted on their mortgage is adversely affected by (2).

Prospective homebuyers whose value has largely fallen off the market due to rising borrowing costs are finding new hope as interest rates begin to decline. As fixed mortgages begin to reflect expected discounts through lower bond yields, a gradual improvement in affordability is expected (3). But buyers should use caution consider their financial strength carefully, as even a small discount may still be higher than historical averages.

Investment rates are also poised to fluctuate with interest rates. While mortgages and investments have struggled in recent years due to higher rates, the expected discount could breathe new life into these assets (1). Real Estate Investment Trusts (REITs), utilities and finance that have been adversely affected by the high interest rate environment, can present attractive investment opportunities as rates fall.

Interestingly, the impact of prime rates on investment decisions extends beyond traditional assets. As borrowing costs fall, there could be an increase in merger and acquisition activity, particularly in real estate. Here large investors have already shown renewed interest in profiting from the price cuts (1).

Even though of the possible effects, 2024 will see the prime rate Realty as an issue to be tackled with some caution and being on guard. The Bank of Canada has signaled that while it has intentions of achieving the policy it will likely happen in a gradual and sensible manner as it enters the red lights. According to the economists output could be acted by 100 basis points by the end of 2024. This is a result of shifting of inflation rate of 8% (1). The prime rate drops down by approximately 6%. Nevertheless, a costly borrowing remains after the period of pre-pandemic compared to that time.

As a final thought, the forthcoming prime rate decline is undoubtedly an important shift for the Canadian economy which would lead to favourable growth. It can give a “peak of hope” for everyone – homeowners and their probable buyers/investors. However, while taking risks and changing this new reality, just being able to adapt is to be expected. The balancing beam also closely depends on this situation. Through staying current, experienced advising, and continuing a long-term strategy, Canadians are able to thrive even in the unforeseeable Prime rate change.

Sources:

(1) https://financialpost.com/investing/interest-rate-cuts-story-2024-mortgages

(2) https://www.ratehub.ca/prime-rate

(3) https://www.moneysense.ca/spend/real-estate/mortgages/fixed-or-variable-mortgage-rate/