The Canadian housing market has undergone major changes in the face of the COVID-19 pandemic. In this case, fluctuating interest rates and changing economic conditions reshaped the landscape. Understanding prime rate trends and their impact on the housing market is important for homebuyers and sellers alike. This article delves into the predictions and strategies of the post-pandemic housing market.

Market Recovery and Pent-up Demand

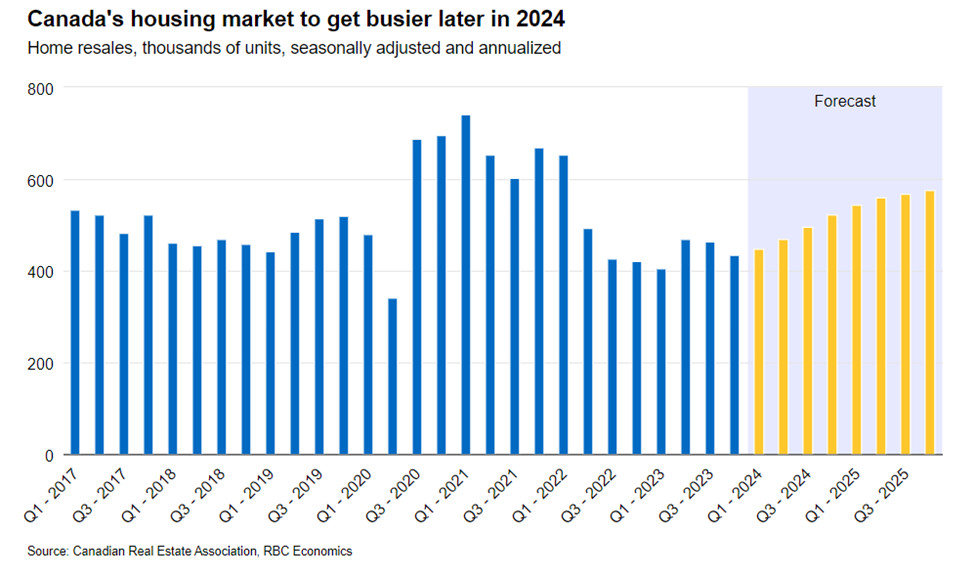

As interest rates begin to decline in the second half of 2024, activity in the housing market is expected to recover. The market projects an annual recovery of 9.2% in home resale in Canada, reaching 484,400 by 2024, with a partial reversal of 25.1% in 2022 and 11.1% in 2023. However, that growth this will be done gradually, so that liquidity becomes easier It will continue to control the overall capacity of the market.

Regional Variations and Resilience

The recovery of the housing market will vary from region to region, with some communities showing greater resilience than others. Alberta, Saskatchewan, Manitoba and much of Atlantic Canada remain close to or above pre-pandemic levels in those markets, while British Columbia and Ontario found a home, the study reveals severe resale crisis as homeowner costs declined.

Price Moderation and Affordability Challenges

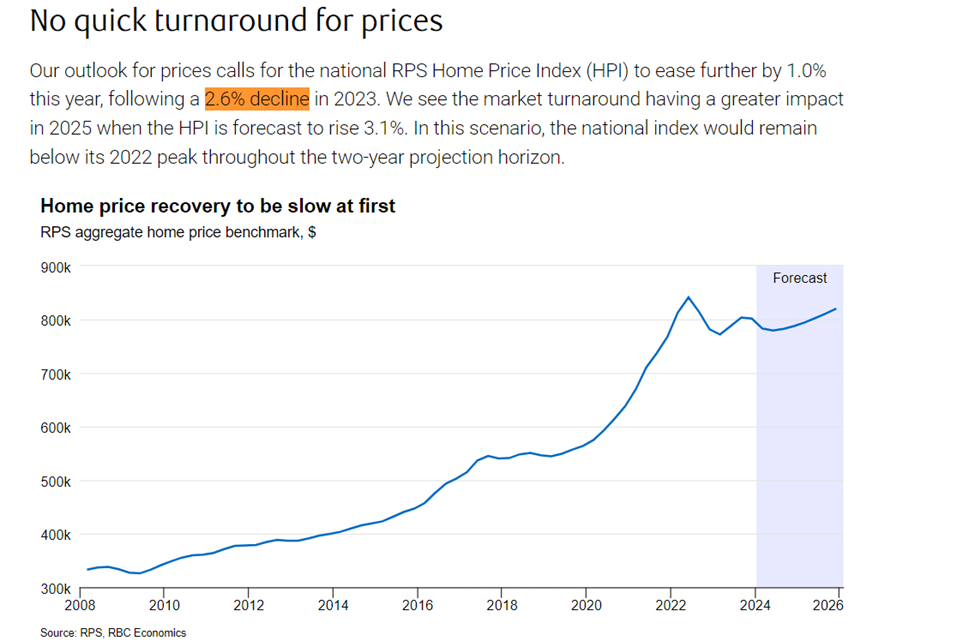

While the housing market will slowly recover, the road to affordability will remain difficult. Market analysts forecast that the National RPS House Price Index (HPI) will decline by 1.0% in 2024 on a 2.6% decline in 2023. However, prices are expected to rebound significantly in 2025, which is expected that HPI will rise 3.1% It forecast.

Inventory Challenges and Supply Response

One of the key factors affecting the recovery of the housing market is the availability of inventory. Continued challenges have been addressed in the lowest housing units, particularly in foreclosures, which has supported demand and driven house prices significantly higher.

To address this issue, market experts emphasize the need for a significant increase in the supply of housing units. It is estimated that Canada needs to increase its housing supply by an average of 315,000 housing units per year by 2030. However, this goal may be difficult to achieve due to labor shortages and other problems faced by the construction industry.

Mortgage Renewal Challenges

Another factor that could affect the housing market in 2024 is the sharp rise in payments awaiting fixed-rate mortgage holders at a later date. They acknowledge that this payment shock is likely to force some owners to sell. But it also means that the risk of a wave of distressed sellers is prohibited by stringent stress testing practices by lenders.

Navigating the Post-Pandemic Housing Market

As the Canadian housing market moves into a post-pandemic environment, homebuyers and sellers need to be vigilant and adapt their strategies to changing circumstances. For prospective buyers, a gradual decline in interest rates in the second half of 2024 may present opportunities, but affordability challenges will remain, and will require they budget carefully and take a long-term view.

On the other hand, sellers will benefit from the anticipated recovery in demand, but many owners will also have to prepare for potential increases in inventory by putting their properties on the market Price strategy its market timing will be critical to maximizing returns.

Thus, the Canadian housing market in 2024 is expected to feature slow recovery, regional diversity, and affordability and ongoing inventory challenges If prime rate trends are made known, market forecasting, and strategic thinking to successfully navigate this challenging terrain.