Protecting your financial future is a top priority for many Canadians, and Guaranteed Investment Certificates (GICs) offer a safe and reliable investment. With banks and financial institutions offering competitive GIC rates, it is important to understand how to navigate the market and choose the best options to maximize returns. In this article, we will examine the key factors to consider when choosing the number of GICs across Canada.

Understanding GICs

Before we dive into the best GIC rates, let’s first understand what GIC is. A GIC is a guaranteed certificate of deposit, an investment with a guaranteed rate of return for a specified period of time. It is considered a safe and relatively low-risk investment,” according to the Bank of Canada. (Source 1)

GICs are especially useful if you have short-term investments, don’t want to be tempted to spend your money, or don’t want to risk investing your money, says the Canadian Financial Consumers Association. (Source 1)

Highest GIC Interest Rates (Non-Redeemable)

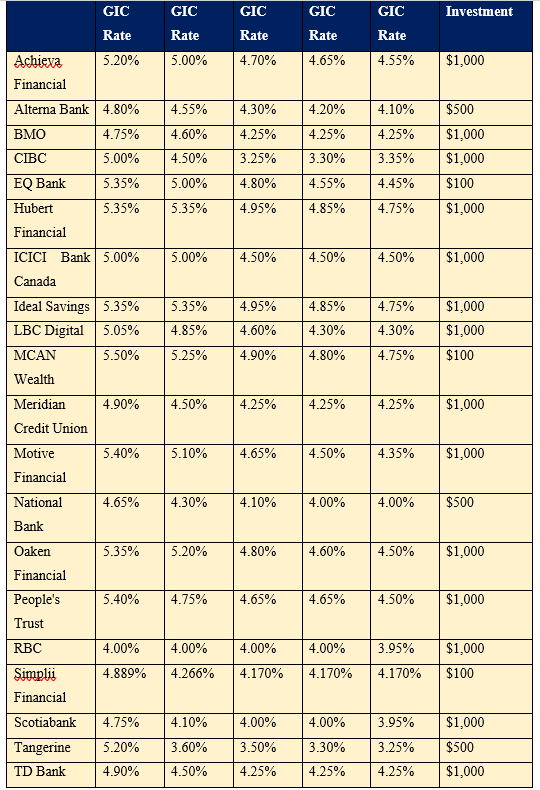

According to Source 1, here are the highest non-redeemable GIC rates in Canada:

Table: GIC rates offered by various providers in Canada for different term lengths, along with the minimum investment required.

Best 1-year GIC: 5.50% at MCAN Wealth

Best 2-year GIC: 5.35% at Hubert Financial and Ideal Savings

Best 3-year GIC: 4.95% at Hubert Financial and Ideal Savings

Best 4-year GIC: 4.85% at Hubert Financial and Ideal Savings

Best 5-year GIC: 4.75% at Hubert Financial and Ideal Savings

Comparing GIC Rates Across Canada

The Market Researcher report provides a comprehensive comparison of Canadian GIC prices (irredeemable and unlisted) over a popular length of time. This table allows you to compare fees from different providers and choose the one that best suits your needs, as recommended by the Canadian Association of Bankers. (Source 1)

The Importance of GIC Insurance

In Canada, GICs are insured by the Canada Deposit Insurance Corporation (CDIC), a government Crown entity that insures eligible deposits up to $100,000. This type of insurance ensures that your deposits are protected. (Source 1)

Strategies for Maximizing GIC Returns

GIC Laddering

The concept of GIC laddering is a method of splitting your money into multiple GICs with different maturity dates. This option allows you to periodically access your investments after GIC maturity, while also applying a higher interest rate, as recommended by the Banking Industry Regulatory Organization of Canada (IIROC). (Source 1)

Registered vs. Non-Registered GICs

There is a difference between registered GICs and non-registered GICs. Registered GICs offer tax-free interest, but you must comply with contribution limits, while unregistered GICs are taxable but have no investment limits, according to the Canada Revenue Agency (CRA). (Source 1)

Exploring 3-Year GIC Rates

As noted by the Canadian Association of Bankers, the analysis of 3-year GIC prices outlines the advantages and disadvantages of these GICs. It includes the security of guaranteed returns along with the predictability of cash flows with standard GICs. Furthermore, it contains the potential for high returns on a GIC types in relation to market. (Source 2)

Alternatives to GICs

While GICs indicates offer quite safe investments, they also need short-term GIC, high-interest bank accounts, bond products and stock market investments as well. Each option offers its own risk profile, funding levels and returns. These may meet different investor’s needs and their investment objectives. (Source 2)

Conclusion

Protection of your future with the best GIC rates requires a detailed research and your risk tolerance of investment targets. With the concepts of GIC options, rates, and strategies, you can make informed decisions for maximising your assumed return while minimizing risk. However, it is necessary to take the consultation of financial advisers for updates on the latest GIC prices. It can ensure that you are making the most of your investments, as recommended by the Canadian Securities Authorities (CSA).

Sources:

https://www.ratehub.ca/gics/best-gic-rates

https://www.forbes.com/advisor/ca/banking/gic/best-3-year-gic-rates/